Markets in Crypto Assets

Preparing for the landmark EU regulation.

Authors

Figure 1: Number of CASP registrations per country

(as of 20/04/2023)

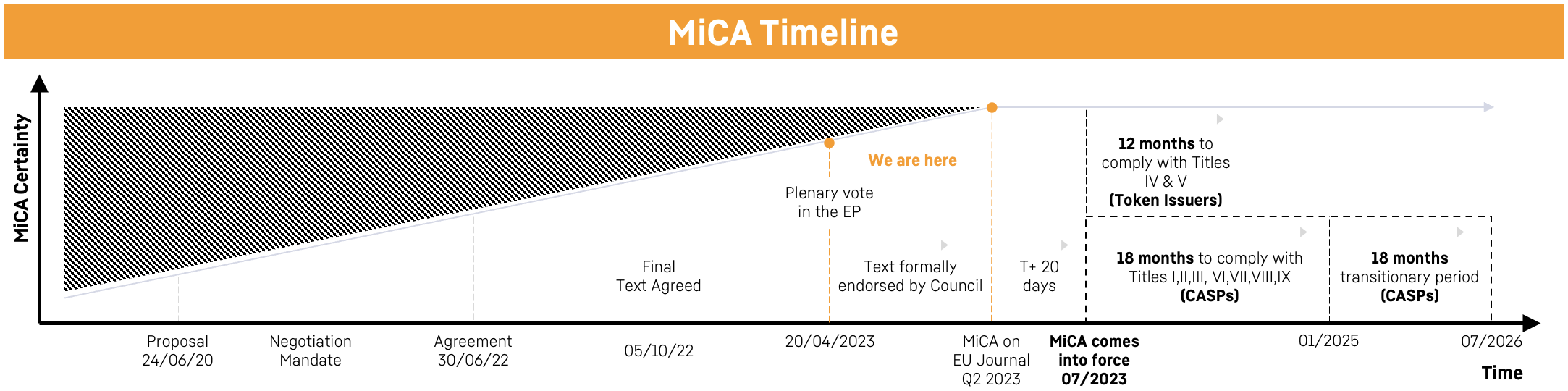

European Union lawmakers approved the landmark licensing law known as Markets in Crypto Assets (MiCA) in a plenary vote on 20 April 2023. Europe is now the first major global jurisdiction to install a comprehensive regulatory framework for the crypto sector, which represents an important step towards bringing greater clarity to the crypto asset market and service providers.

Prior to MiCA, Europe was a fragmented and uncertain environment for crypto-orientated firms, with over 50% of member states requiring their own, country-specific Crypto Asset Service Provider (CASP) registrations for CASPs to actively operate in that market.

MiCA regulation is the European Parliaments’ solution to the disjointed CASP registration process across EU member states. The legislation will reform Europe's stance on crypto assets and harmonise its regulatory approach across the entire EU jurisdiction.

MiCA will require all CASPs, including exchanges, wallet providers, and custodians, to obtain a license and comply with a range of requirements. These requirements aim to promote innovation while ensuring all CASPs are held to adequate operational, governance, prudential, and consumer protection standards.

Preparing for MiCA

Becoming compliant with MiCA will require organisation-wide efforts, which, depending on a firm's regulatory status and organisational readiness, may entail significant preparation and/or remediation. Firms seeking MiCA authorisation should act early and allocate sufficient time to ensure compliance and allow themselves to capitalise on strategic opportunities from being a first mover in achieving EU-wide authorisation. Preparing for MiCA regulation will require a proactive and thorough approach. Here are some steps CASPs can take to get ready:

Understand the MiCA text

CASPs must familiarise themselves with the comprehensive MiCA legislation, its nuanced scope, and operational requirements. Firms may wish to seek advice to ensure they fully understand the regulation and the requirements it imposes on them.

Gap analysis

Once a firm understands how MiCA applies to them, they must conduct a thorough readiness assessment in preparation for the legislation’s entry into application.

Licensing process preparation

For both existing firms, and new firms not yet regulated in Europe, the MiCA application process will involve assessing which member state to choose as its operational base and, thus, which competent authority (national financial supervisor) to seek MiCA authorisation from. This is an important decision for firms and should be assessed carefully across a range of criteria, including a firm's existing operations, regulatory status and relationships, language capabilities, and their strategic priorities (e.g., speed to market) as well as a country's regulatory perception and attitudes.

CASPs should begin preparing for the licensing process as soon as possible. They should ensure they have all the necessary documentation and information required for the license application and that they are prepared to demonstrate compliance with the regulation's requirements. Previous MiFID, Banking, and or EMI licence application experience is likely to give a firm an indication of the substance required to be authorised, although the finer details remain uncertain until official application and assessment processes are released.

Implementation programme mobilisation

Once crypto asset service providers have mapped MiCA's requirements to their firm and identified gaps in their compliance measures, they should mobilise a MiCA programme to implement any necessary changes to ensure they are fully compliant with the organisation-wide requirements.

Long-term strategic vision

The crypto service provider’s market is becoming increasingly crowded, and MiCA will level the playing field for those firms who achieve authorised status. An effective market strategy, product proposition, and long-term strategic vision are imperative. CASPs should embrace the reality of the competitive landscape and create a resilient strategy for a volatile market. Product innovation and revenue diversification can help decouple a firm’s performance from market conditions – lessening the dependency on crypto asset price appreciation.

How Valentia Partners can help

Our Fintech Consulting practice is assisting Financial Institutions and Crypto Exchanges to deliver transformation leveraging crypto technologies. Get in touch to find out more.

Valentia Partners supports crypto exchanges, custodians, and incumbent Financial Institutions to navigate this youthful industry and anticipate the evolving regulatory landscape. Operating at the intersection of Financial Services & FinTech, we bring together deep industry expertise and insights to shape incumbents’ innovation agenda and support Fintechs to scale and succeed.

We have helped CASPS successfully navigate towards EMI licences and EU CASP registrations (including the first-ever Central Bank of Ireland CASP approval). Additionally, Valentia has a depth of experience across Financial Services regulation, including MiFID II operational setups for large banking players.

MiCA is a new regulation with nuanced and discrete implications separate from other European regulatory frameworks that firms must also be cognisant of, including the existing EU AML/CFT, TFR, and MiFID II frameworks. Since the agreement of the final text, Valentia Partners has built a MiCA breakdown pack that synthesises the key strategic and operational considerations for firms and can help map the path to effective compliance. We detail MiCA’s origins, goals, rules for CASPs and token issuers, and our thoughts on MiCA’s impact on the European market landscape.

If you are a CASP wishing to succeed in the current crypto landscape and attain regulatory permissions underpinned by a growth-focused and robust operating model, reach out to one of the Valentia Partners team and ask about our MiCA readiness assessment.

Related Articles