ESG as a risk management framework for secured lending

The combined effects of climate change, socio-economic change, and the shift towards a more credit driven economy expose lenders to greater and more diverse risks than ever before. ‘ESG’ provides a framework that enables sustainability analysis.

Downloads

Authors

Re-framing ESG as the ultimate exogenous- risk management framework

The combined effects of climate change, socio- economic change, and the shift towards a more credit driven economy expose lenders to greater and more diverse risks than ever before. Environmental, Social, and Governance (ESG) hands them a ready-made framework for exogenous risk identification, evaluation, and management.

Historically lenders have focussed on streamlining evaluation rather than including comprehensive ESG risks in the secured lending approval and review processes. Although banks conduct checks on the sustainability of the companies and collateral they lend against, a great deal of insight is left on the table. By fully leveraging the ESG framework and available sources of data alongside modern data processing capabilities banks can vastly increase the range of risks they evaluate, price against, and mitigate to achieve sustainability across their loan-books.

Inclusion of ESG factors in the European Banking Authority's (EBA) pillar 3 reporting points directly at opportunities to improve existing risk assessments. These opportunities have far reaching implication on collateral values, borrower obligations, and the aggregate stability of the lending industry. Banks and lenders can fortify debt values against climate risks, social pressures and the need for robust, careful and diligent governance.

Valentia Partners believes that those lenders who prioritise building their lending processes around ESG factors early will reap rewards in the long run. By conducting initial, tactical review of existing lending creditors can feel-out those data sources, processes and analyses that need to be included in strategic operating model change.

Uncovering ESG Risks:

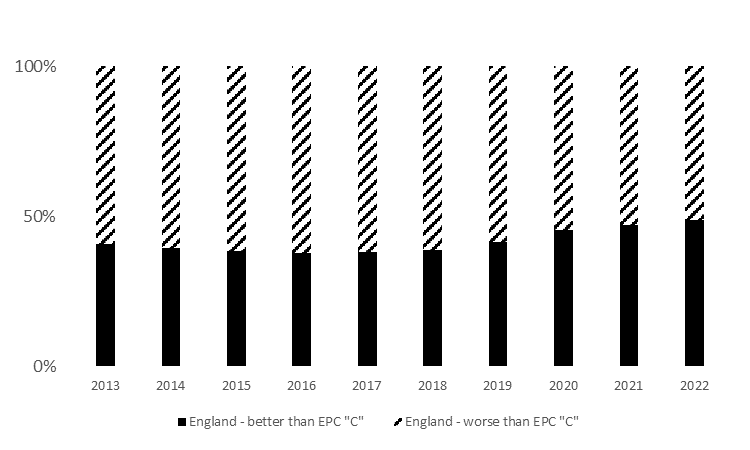

Figure 1: Proportion of English housing meeting EPC ‘C’

Figure 2: Housing un-affordability ratio, 1997 to 2022

In the UK and Ireland increased comprehension of changing economic landscape and its relationship with climate change, social change and monetary policy are leading lenders to question whether some secured lending is currently overvalued. The shifting landscape of sustainability, climate risks, and social factors poses a direct threat to collateral values and borrower capacity, presenting clear opportunities to enhance the way lending is assessed.

Sustainability Impact: New rules for landlords require that rental property in the UK exceeds an Energy Performance Certificate (EPC) rating of 'C' by the end of 2028. This will require substantial investment in meeting energy standards. For landlords, failure to comply will mean income from real-estate assets disappears and the market value of non-compliant properties is likely to drop. For lenders this could mean de- valued collateral and defaulting borrowers.

Climate Risks: Increased incidence of extreme weather events due to climate change increases risk to banks. The impact of natural disasters will reduce the value of real-estate collateral and could drive default risk through borrower distress. The Bank of England (BoE) climate stress test has projected substantial mortgage losses, estimating a 40% increase in mortgage losses in the early action scenario and 164% under the late action path over the 30-year assessment period.

Social Factors and Defaults: In the UK, the average house-price-to-earnings ratio has doubled over the past 20 years, with certain regions such as London reaching a staggering ratio of 11. The impact has led to significant financial strain for borrowers as their financial circumstances have evolved since they obtained their loans. Rising inflation has further exacerbated the challenges faced by borrowers, compounding their financial difficulties, and increasing the risk that they can no longer afford to make repayments.

ESG's Influence on Mortgage Values in the UK & Ireland:

Below follow some example statistics describing the challenges ahead for secured lending in the UK.

Sources: 1. CRED (2020) , 2. Morgan Clark (2020), 3. Open Property Group (2022) , 4. Centre of Ageing Better (2022) & 5. JRF UK Poverty Report (2023)

A similar situation will play out In Ireland.

Sources: 1. Gamma Flooding & Climate Report (2020) , 2. Gamma Flooding Report (2020) , 3. Central Statistics Office - BER Assessment (2018), 4. Central Statistics Office - Poverty Rate (2022), 5. Housing to Income Ratio

Factors related to the ESG framework are set to have a substantial impact on secured lending in the UK and Ireland.

Failure to address these risks threatens substantial losses and reputational damage for banks. The ESG framework and associated data present an opportunity for creditors to get ahead of these risks and ensure that, at the very least, they are prepared for the challenge to come.

Mitigating E&S Risks for Banks:

Valentia Partners recommends that banks take steps to mitigate ESG risks across their lending practices. Although comprehensive adoption of front-to-bank sustainability assessment will be dependent on sector and business plan we can point to some case-studies of how building-In ESG will mitigate emergent risks.

Inadequate Energy Performance: Banks can incentivize energy-efficient upgrades by offering preferential loan terms or lower interest rates for properties meeting specific EPC requirements. Where creditors find they have existing lending against Inefficient housing-stock it may make sense to support debtors in funding the efficiency improvement investments needed.

Impact of Storms & Floods: Climate risk assessments need to be integrated into the Bank's loan underwriting process to identify properties

in high-risk areas prone to storm and flood damages. Where existing lending is discovered against high-risk property a pricing evaluation is needed and hedging against default may be wise.Unaffordable Housing and Mortgage Defaults: Short-term or point-in-time affordability assessments no-longer stand up in the rapidly changing economic landscape. Banks must take steps to ensure that lending practices are sustainable in several interest rate stress scenarios. Tactically banks can avoid reputational risk by seeking to support borrowers who find themselves in financial distress.

To effectively address and mitigate each of these risks, banks must embark on a comprehensive organizational effort to integrate ESG elements into their origination and approval process. This entails embracing a holistic approach that involves acquiring and analysing the latest and most relevant ESG data points specific to their company's operations.

It is no coincidence that the data required to effectively evaluate the sustainability of secured lending is the same data that the EBA and others are expecting Banks to report on a regular basis. Identifying, sourcing, and integrating this data early will position lenders for seamless compliance as the time comes.

In delivering both compliance and enhanced analytics banks can gain valuable insights to inform their decision-making and enable them to proactively manage ESG risks in a manner that aligns with their long-term sustainability goals. Enhanced forecasting will enable bank to take more targeted treasury decisions that reduce the cost of capital whilst also driving down the cost of borrower defaults.

Leveraging Valentia Partner's Expertise In E&S Risk Mitigation:

To discover more or talk to us about anything you've read here please don't hesitate to get in touch.

Valentia Partners extensive experience handling existing loan books and our data and enterprise architecture expertise position our SMEs uniquely to support lenders in scoping, designing, engineering, and delivering analyses of existing lending. The firm's strategy and operating model experience combine to enable us to help your organization convert that analysis into long-term value.

Valentia Partners deliver from 'Thought to Execution' meaning we'll be with you every step of the way.

Understanding Current Practices: Evaluating existing methods of incorporating ESG into valuations and risk assessments, targeting areas for Improvement that balance Immediate benefit realisation and long-term strategic value.

Designing a Best-in-Breed ESG Risk Assessment: Bespoking a robust ESG risk assessment framework that aligns with industry standards and regulatory requirements and enables you to evaluate the full range of ESG risks associated with your lending practices and business plan.

Acquiring and Analysing ESG Data: Collaborating with a trusted network of data vendors to source appropriate ESG data. Allowing banks to evaluate ESG performance and potential risks in their loan portfolios by building on the ESG risk assessment and conducting analysis for actionable Insights.

Delivering Long-Term ESG Integration: By leveraging advanced analytics techniques, banks gain insights into ESG risks and opportunities, empowering informed decision-making and enabling adjustments to lending terms, interest rates, or commercial strategies. Addressing strategic, operating model components in light the ESG framework lenders can build more sustainable practices.

Valentia Partners can support your organisation in delivering long-term sustainability.

Related Articles